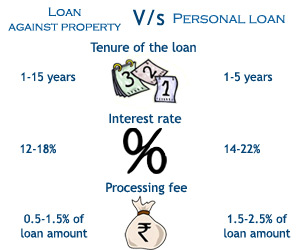

Each one of us at some point of our lives faces financial glitch. The reason might be whatever; it is always a heavy burden on the shoulders. Expecting help from friends and family is obvious but what if the amount exceeds their limit. The money crunch is one of the hardest to fall on you and it’s always better to find an intelligent solution to come out of it. Taking a personal loan is a good option. However the rate of interest is extremely high adding to the less tenure of return of loan amount. Here loan-against-property takes the entry. An asset like your house or a property you hold can be effectively used as a tool for obtaining a loan. It has multiple plus points when compared to personal loan. Moreover it can offer you about 70% of the value of the home (on against which you are acquiring loan). This is because it is a secured loan; you are putting the value of your property here, whereas the personal loan is a totally unsecured loan.Loan against property gives you a much longer tenure of paying back the loan. Typically its 1-9 years but some banks may extend to 15 years if the amount is heavy while personal loans avail only 1-5 years of tenure. The interest rate varies from 12-16 %, way lower than personal loan that proposes 14-22% interest rates.How to obtain a loan against property?

Each one of us at some point of our lives faces financial glitch. The reason might be whatever; it is always a heavy burden on the shoulders. Expecting help from friends and family is obvious but what if the amount exceeds their limit. The money crunch is one of the hardest to fall on you and it’s always better to find an intelligent solution to come out of it. Taking a personal loan is a good option. However the rate of interest is extremely high adding to the less tenure of return of loan amount. Here loan-against-property takes the entry. An asset like your house or a property you hold can be effectively used as a tool for obtaining a loan. It has multiple plus points when compared to personal loan. Moreover it can offer you about 70% of the value of the home (on against which you are acquiring loan). This is because it is a secured loan; you are putting the value of your property here, whereas the personal loan is a totally unsecured loan.Loan against property gives you a much longer tenure of paying back the loan. Typically its 1-9 years but some banks may extend to 15 years if the amount is heavy while personal loans avail only 1-5 years of tenure. The interest rate varies from 12-16 %, way lower than personal loan that proposes 14-22% interest rates.How to obtain a loan against property?

- The first thing you should care about is if it has more than one owner. If it has, then all the owners will become joint applicants in acquiring the loan.

- The loan can be acquired against any kind of freehold property. It doesn’t matter if it’s a house or a plot, if you live in it or rented it. If you own the property then you can use it for loan.

- Make sure the property is clean and doesn’t carry any encumbrances otherwise the bank may reject the plea.

- The bank will scrutinize all the documents including the proof of residence such as ration cars, electricity bill or telephone bill. Along with that you have to produce proof of identity (voter ID, passport, PAN card).

- If you are employed then the bank will ask for bank statement of the past six months. If self employed then furnish a certified financial statement for past two years.

- The loan varies from person to person depending on work profile and age of borrower. Also the bank asks for three years of income proof hence the minimum age to apply for it is 24 years. It goes to 60 for a salaried person and 65 for self employed.

- The bank also confirms your credit history and repayment rack record through CIBIL. If there is some fault in any bill payment then it will reduce your chances of getting a loan.

- After the final scrutiny of all the documents, around 40-70% of the value of property will be sanctioned.

How wise it is to take a loan against property?There is no doubt that taking a loan against property is much more profitable than a personal loan. But they why people fear to step for it?The answer is the risk. Most of us don’t want to take the risk of bank taking over the property if we are unable to pay the dues. So our conscience shakes and we prefer not to enter this dangerous decision. Another disadvantage is that this loan gives no tax incentives while paying the EMI, unlike in home loans. However a businessman can claim tax deduction on the interest rates if he can prove that loan was used for the betterment of business.It cannot be denied that it’s a risky way of getting loan but it is cheaper and better than personal loan in many ways. займ на карту без отказов круглосуточновзять кредит онлайн